Consider a scenario of two people: each 25 years old, David who makes $40,000 a year and Michael who makes $80,000 a year. Each year, they get a 2.5% raise and both work until they are 73 (yeah, this might be the regular retirement age twenty years down the road, thanks to demographic changes and improved healthcare).

Let’s say the only difference is that David starts saving 10% of his income when he’s 25, but Michael decides to wait until he’s 40 while he’s making $115,000 a year.

Let’s also err on the conservative side of things and say that money grows in the stock market at an annual rate of 7% each year, which is actually slightly less than the average historical annual return of the Singapore STI and the S&P 500.

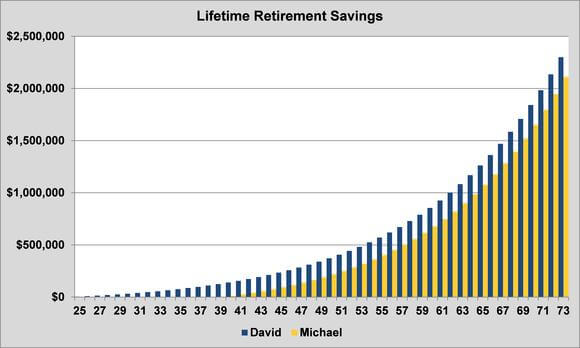

By the time each is 50, they would’ve each taken a little more than $144,000 out of their paychecks and put it towards retirement. But when they retire at 73, do you know who would end up with more money?

Despite earning half as much money over the course of his lifetime, David would end up with roughly 10% more than Michael. David would have $2.3 million in savings when they retire, whereas Michael would have $2.1 million:

What is even more remarkable than David ending up with more money, despite earning half as much in salary is that ultimately Michael even saved 60% more money than David (roughly $610,000 in savings for Michael, versus $375,000 for David).

If you decide to get ambitious and say that money grows at 8.5% a year, David actually ends up with almost 30% more than Michael, with $3.7 million in savings, versus $2.9 million.

The magic of compounding at work.